Global inflationary pressures are finally waning. As this relief comes after months of monetary policy tightening, one might be tempted to draw a direct line between higher interest rates and lower inflation rates. But correlation does not necessarily imply causation. I believe that inflation would have come down even in the absence of aggressive tightening measures – with one important caveat.

1. Inflation trending lower

Global inflation rates, while still being elevated, have been trending lower for several months now. In the US, which is once again leading these developments, the 12M increase in the CPI consumer price index already peaked back in mid-22, with European countries following one to two quarters behind. What’s more, short-term developments, such as the 3M changes in the CPI are pointing to further and even more pronounced declines in inflation rates, boding well for the inflation outlook.

As the inflation peak roughly coincides with the start of aggressive monetary policy tightening measures by global central banks (the Federal Reserve lifted its target rate for the first time in March 2022), one might be tempted to draw a direct line between higher interest and lower inflation rates. But correlation does not necessarily imply causation. I strongly believe that inflation would have come down even in the absence of aggressive tightening measures – with one important caveat.

2. Rise and fall of supply constraints

The rationale behind my thinking is that the bulk of the inflation surge was caused by supply-side factors (bottlenecks, higher commodity prices, etc) rather than by strong underlying demand. Likewise, it is now the fading of those supply constraints that has been driving inflation rates lower. The following two charts vividly illustrate the dramatic rise and fall of global supply chain factors that first drove up costs and prices and have now dropped back to or even below their longer-run averages:

This gallery could easily be extended with charts of energy prices (oil or gas), prices for food or for cars. All of them have dropped sharply from their elevated heights reached either during the first months of the war in Ukraine or post-Covid.

The one important features that these „corrections“ have in common is that none of them hav been caused by higher interest rates. Instead, it was a combination of fading external shocks and the normalization from exaggerated upturns that brought these indexes down again. And that, in my view, would have happened just as much and just as fast in the absence of higher interest rates. After all, monetary policy cannot directly impact the supply side of the economy.

„Wait a second!“, you might now argue. Of course can monetary policy impact the supply side. Because when higher rates only curb demand strongly enough, supply-side pressures will automatically ease as well. The only problem with this – theoretically sound argument – is that it doesn’t hold empirically (New York Fed researchers Benigno et al. (2023) analyzed the impact of demand factors to the Global Supply Chain Pressure Index. They found that „Over the course of late 2020 through the first three quarters of 2021, global demand factors contributed positively to global supply pressures, but the contributions were relatively modest relative to the overall magnitude of supply factors.„)

3. Tighter monetary policy has (so far) not affected demand

The first chart, which is taken from the New York Fed’s bi-weekly Oil Price Dynamics Report, reveals the contribution of supply and demand factors to the change in oil prices. As can easily be seen, it has been the supply side (red line) that initially caused the sharp rise in Brent (reflecting fears of energy shortages at the beginning of the war in Ukraine) and has now also been the key driver of lower oil prices. The contribution of demand factors (light blue), on the other hand, has been much more stable over the past two years.

Next, we turn to the labor market, which usually plays a critical role for the transmission of monetary policy changes to the real economy and prices. the chart shows that there are currently still 1.9 job openings for each unemployed person. While that admittedly is a bit lower than the 2.2 reached last June, this number has remained way higher than at any time during previous cycles. According to this ratio, which Bernanke and Blanchard (2023) in their recent paper use as their preferred measure of slack, tighter monetary policy has thus not yet hit labor market dynamics in any meaningful way. Other figures, such as payroll gains or the jobless rate, corroborate that notion.

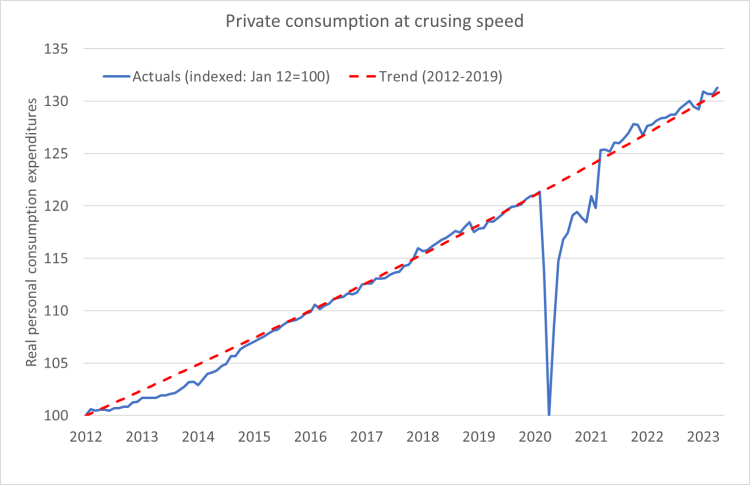

Along the same lines, we do not find any meaningful impact of higher interest rates on consumer spending. Not only has remained nominal spending inflated (courtesy of higher prices), but is price-adjusted real consumer spending very closely tracking its longer-run trend. This is remarkable given all the headwinds that the consumers have been facing in recent months, but the strong labor market and savings involuntarily built-up during the Covid months have helped households to weather the storm. To be sure, there has been a shift below the surface from weaker goods demand, which rebounded post Covid and has since eased again, to stronger spending for services. Nevertheless, overall demand by households has not taken a hit from higher rates.

Another interest rate-sensitive sector of the economy ist housing. Here the verdict needs to be a bit more differentiated. Because on the one hand we already see the significant damage that higher rates have done, as house prices and construction activity having plummeted in recent months. At the same time, however, the shelter index in the CPI has actually continued to accelerate. As I argued in my previous note, this index has even been the main reason, why US inflation had remained stubbornly high. So, while tighter monetary policy absolutely has negatively affected the housing market, this slowdown did not (yet) enter the CPI. It thus does not explain the slowdown in inflation rates, either.

4. The (important) caveat: inflation expectations

To summarize my previous thoughts: Higher interest rates are not the main driver behind the slowdown in inflation rates, as demand and typically interest-rate-sensitive sectors have remained fairly robust of late. Instead, price pressures moderated primarily thanks to fading supply-side shocks.

It may now seem contradictory, when I add that in my view it still was the right thing to do for central banks to start hiking. First, we must not forget that the monetary policy stances of most central banks around the globe were extremely easy in early 2022, after they went all-in again during the Covid-crisis. So, what they really did was not to tighten but to remove accommodation. And while for some, this might merely be a semantic difference, the second point really matters: Central banks had to act in order to show market participants their commitment to bring inflation down. Fundamentally, this is of course a bit tricky, if higher rates only have limited impact on the supply-side disruptions … but had they done nothing, markets might well have lost faith in the Fed and other central banks. The result could have been a devastating unmooring of inflation expectations.

Stable inflation expectations were and are arguably one of the main assets that central banks had in recent months. Because despite the fact that inflation rates were too high for too long, longer-run inflation expectations remained well-behaved, thus working as the much-needed anchor. It has taken decades for central banks to gain that trust – and they desparately needed to defend it. (San Francisco Fed President Mary Daly made a similar point here). If inflation expectations had risen too much, things could have easily spiralled out of control (yes, much worse than what we saw) and it might have needed a Volcker’ian effort to bring inflation rates and expectations back down to earth again. Luckily, it seems that the Fed and other central banks succeeded – which brings me to my last point: this impending success has been emerging for some months now – even as inflation rates (which are 12M changes in an index) continued to be high. So while I think that raising rates was the right thing to do, I still wonder whether it has been necessary to continue to tighten at such a rapid pace and causing collateral damage such a some bank failures in the US along the way.

Ein Kommentar zu “Correlation does not imply causation: the case of higher interest and lower inflation rates”